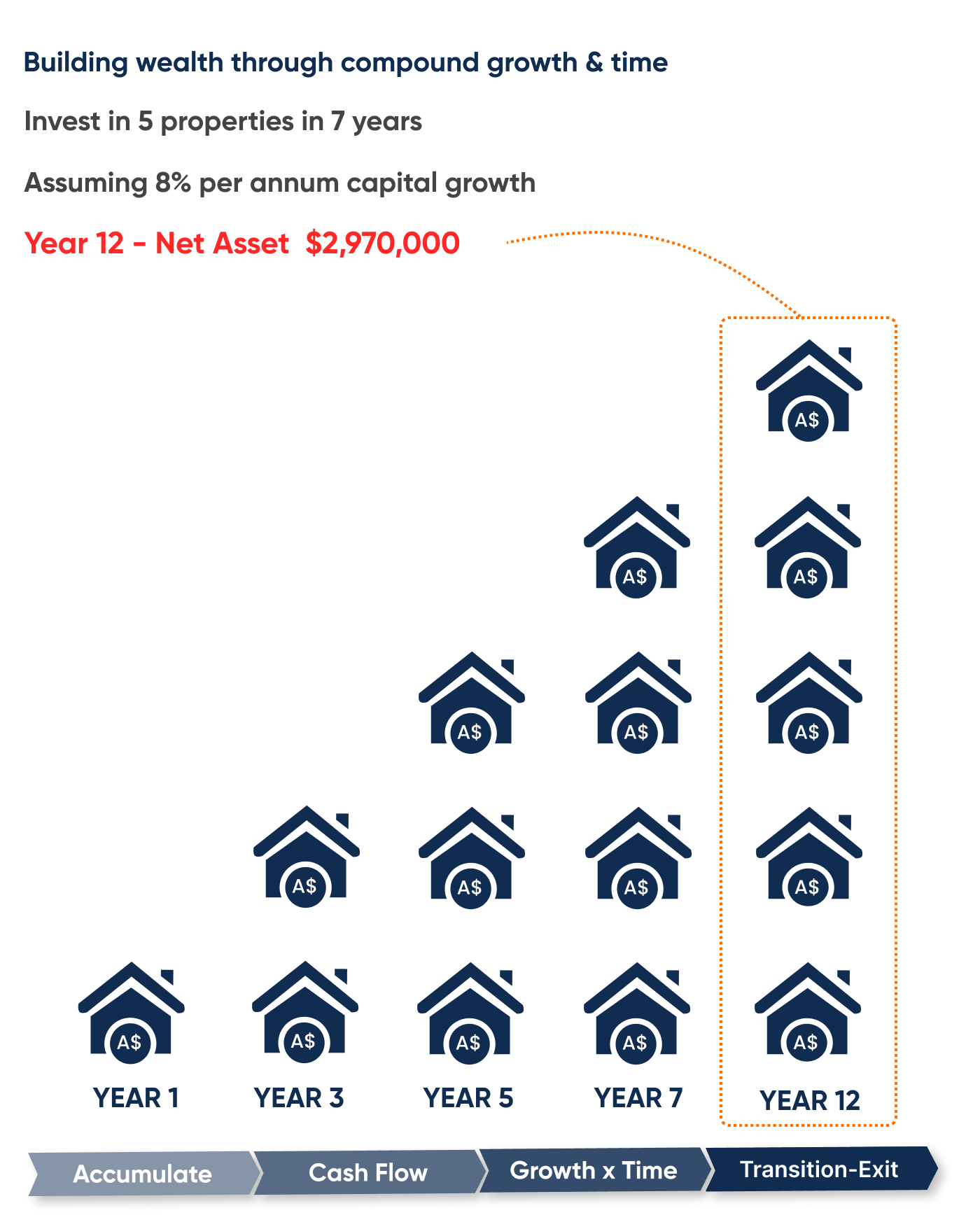

Introduction

In Australia, more individuals, couples, and families are turning to investment properties as a pathway to long-term security and financial freedom. The appeal lies in generating passive income from rental income, creating stability without reliance on traditional employment. Yet the pressing question remains: “How many investment properties do I need to retire comfortably?” The answer depends on your property investment strategy, lifestyle goals, and how well your investment portfolio is managed. With tailored guidance from experienced financial advisers, achieving retirement security through property investment is possible.

What Does It Mean To “Retire” With Investment Properties?

Retiring with property means replacing active income with cash flow from a well-structured property portfolio. The focus is on consistent rental yield, long-term capital growth, and maintaining a balance between mortgage repayments and rental property performance. This approach provides:

- Financial independence

- Time freedom to pursue personal goals

- Wealth preservation through rising property values

To succeed, investors must monitor the property market, track changes in interest rates, and anticipate challenges like capital gains tax when selling assets.

The Core Formula: Calculating Your Target Number

The fundamental calculation is:

Number of Properties Needed=Desired Monthly Retirement IncomeAverage Net Monthly Cash Flow per Property\text{Number of Properties Needed} = \frac{\text{Desired Monthly Retirement Income}}{\text{Average Net Monthly Cash Flow per Property}}

- Desired monthly retirement income: Amount needed for lifestyle expenses (e.g., $5,000–$10,000/month).

- Net cash flow: Rental income minus mortgage payments, taxes, insurance, repairs, vacancies, and other costs.

Sample Calculations

| Desired Income | Average Cash Flow per Property | Number of Properties Needed |

|---|---|---|

| $5,000 | $500 | 10 |

| $8,000 | $800 | 10 |

| $10,000 | $1,000 | 10 |

Whether you pursue positive gearing for positive cash flow or negative gearing for potential tax benefits, aligning your strategy with your goals is key.

Real-World Variables That Impact Your Calculation

Key factors shaping your property investment strategy include:

- Property Location: Urban centres may deliver stronger rental yield, while regional hotspots can offer better capital growth.

- Property Type: Houses, units, or short-term rental property options all influence cash flow differently.

- Debt Structure: Balancing loan-to-value ratio (LVR) and debt-to-income ratio (DTI) impacts your borrowing power.

- Expense Variability: Ongoing maintenance, strata fees, and vacancies reduce returns.

- Market Cycles: An interest rate cut by the Reserve Bank of Australia could increase borrowing capacity and boost market value.

Comparative Table: Impact of Property Type and Location on Cash Flow

| Property Type | Urban Area | Suburban Area | Regional Area |

|---|---|---|---|

| Single-Family | High | Moderate | Low |

| Multi-Family | Moderate | High | Moderate |

| Short-Term Rental | High | Moderate | Low |

Investment Rules Of Thumb: 1% and 50% Rules

Two popular rules simplify property evaluation:

- 1% Rule: Monthly rent should equal at least 1% of the purchase price.

- 50% Rule: Expect roughly half of rental income to cover expenses (excluding mortgage repayments).

Applying These Rules

- Calculate 1% of purchase price to set minimum rent.

- Estimate costs using the 50% rule.

- Compare projected cash flow with your goals.

Limitations: Rules are guidelines only. Property research is essential for accuracy.

Funding Your Retirement: Planning and Preparation

To build a strong property investment strategy:

- Capital Requirements: Budget for deposits and reserves.

- Lending Criteria: Lenders assess debt-to-income ratio and serviceability.

- Start Early: Time allows for capital growth and debt reduction.

- Interest-only loans: May improve cash flow, though mortgage repayments remain.

Checklist: Preparing Your Retirement Property Portfolio

- Assess financial position with a financial adviser.

- Conduct thorough property research.

- Work with a buyer’s agent to identify quality assets.

- Diversify to create a diversified portfolio.

- Allow for economic shifts and rental demand changes.

Portfolio Management As You Approach Retirement

Managing your investment portfolio near retirement requires strategy:

- Scaling or Simplifying: Consolidate assets for stability or expand for more passive income.

- Management Style: Weigh active management against outsourcing.

- Family Planning: Consider reverse mortgage or home reversion strategies to unlock equity.

Pros and Cons of Active vs. Passive Property Management

| Management Style | Pros | Cons |

|---|---|---|

| Active | Control, potential savings | Stress, time-consuming |

| Passive | Less stress, more free time | Management fees, reduced control |

Frequently Asked Questions (FAQ)

- How much should I expect in expenses per property?

Around 50% of rental income, excluding mortgage payments. - Should I own many lower-value properties or fewer high-value ones?

Both approaches work. A diversified portfolio balances risk. - Does appreciation matter in retirement?

Yes. Capital growth increases asset value even if you rely mainly on cash flow. - Can I retire with fewer high cash-flowing properties?

Yes, though higher cash flow often comes with higher risks. - What happens during vacancies or downturns?

Maintain reserves and flexible finance structures. - What about tax considerations?

Tax benefits may include depreciation and expense deductions. Seek advice from the Australian Taxation Office or a qualified adviser.

Common Mistakes and How To Avoid Them

- Overestimating cash flow, underestimating costs.

- Excessive leverage without buffers.

- Ignoring interest rate risks.

- Neglecting property research and tenant demand.

Case Studies

Investor A: Retired with four fully paid-off properties, relying on rental yield for consistent passive income.

Investor B: Used the property stacking method, building 10 leveraged properties before consolidating into three high-value ones with strong cash flow and better capital growth.

Both investors achieved retirement security through different strategies aligned with their goals.

Step-by-Step Guide: Building Your Retirement Property Portfolio

- Define your income goals and assess lifestyle costs.

- Estimate realistic cash flow per property.

- Calculate the number of rental properties required.

- Establish an acquisition timeline for buying properties.

- Reassess regularly—monitor property market trends and interest rates.

- Plan for long-term management: self-manage, hire managers, or consolidate.

Final Considerations Before You Retire

- Balance property with other investments like shares or a self-managed super fund.

- Use the AMP retirement calculator to align projections with pension payments.

- Stay educated on interest rates and policy changes from the Reserve Bank of Australia.

- Consider support from a buyer’s agent for future purchases.

- Explore regional hotspots for growth potential.

This guide demonstrates how Australians can retire with property by focusing on cash flow, capital growth, and smart property investment strategies. By managing mortgage repayments, monitoring interest rates, and building a diversified portfolio, you can create reliable passive income and long-term financial freedom.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.