Blog: What Is Debt Recycling? A Comprehensive Guide for Australian Homeowners

Introduction

Debt recycling is a financial strategy that many Australians are beginning to explore as they seek smarter ways to manage their home loan debt, optimise their cash flow, and build long-term wealth creation. For homeowners, the process offers a way to transform non-deductible debt (like your principal residence mortgage) into tax-deductible debt, while also investing in income-producing assets. With the right approach, debt recycling can help you repay your mortgage faster, grow an investment portfolio, and achieve greater Financial Independence. In this guide, we’ll explore what debt recycling is, how it works in an Australian context, the tax benefits, the risks, and whether it might suit your personal financial goals.

Defining Debt Recycling

Debt recycling, sometimes referred to as mortgage recycling, is a process that gradually replaces non-deductible debt (such as a principal and interest loan for your home) with tax-deductible debt used to fund investments. Essentially, you use available equity in your home to borrow and invest in income-generating assets such as Australian shares, Exchange-traded Funds (ETFs), international shares, managed funds, or even investment property loans.

The key idea is that while your mortgage interest payments on your home loan are not tax-deductible, the interest expenses on your investment loan may be eligible for a tax deduction, provided the funds are invested in income-producing assets. Over time, the growth of your share portfolio, rental properties, or other investments may generate investment income and capital gains, all while shifting more of your debt into the tax-deductible category.

Table: Non-Deductible Debt vs. Deductible Debt in Australia

| Type of Debt | Definition | Examples | Tax Treatment |

|---|---|---|---|

| Non-Deductible Debt | Debt where interest is not tax-deductible | Home loan (PPOR mortgage) | No tax deduction on interest payments |

| Deductible Debt | Debt used to acquire income-producing assets | Investment loan, line of credit | Tax-deductible interest under ATO rules |

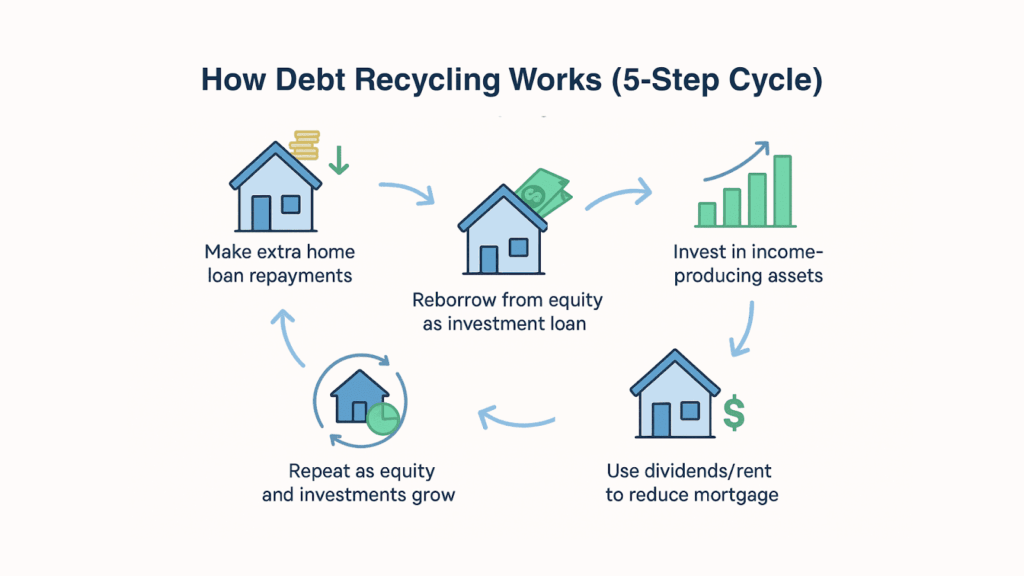

How Debt Recycling Works in Australia

Here’s a step-by-step process of how debt recycling might work for an Australian household:

- Start with Your Home Loan: You begin with your standard principal-and-interest loan. This is a non-deductible debt as the interest payments on your PPOR are not eligible for tax deduction.

- Pay Extra into the Mortgage: Use any surplus cash flow to pay down your home loan debt faster.

- Redraw or Loan Split: Through a split loan, redraw facility, or line of credit, you access the repaid equity and convert it into an investment loan.

- Borrowing to Invest: You direct these borrowed funds into income-producing assets such as managed funds, share market investments, Australian shares, international shares, or an investment property.

- Earn Investment Income: Dividends, rental income, and franking credits from these investments increase your cash flow.

- Reapply the Income: This passive income is then used to pay down more of your home loan, freeing up equity to repeat the cycle.

Note: Using an offset account alongside loan splits can help keep track of deductible vs. non-deductible portions. Always check the tax implications with a financial advisor to avoid breaching Australian Tax Office (ATO) rules, including Part IVA.

Debt Recycling vs. Other Strategies

| Strategy | Approach | Risk Profile | Tax Implications |

|---|---|---|---|

| Debt Recycling | Replaces non-deductible debt with tax-deductible debt while investing | Moderate market risk | Interest on investment loans is usually deductible |

| Equity Release | Accesses home equity borrowings for consumption or investment | Low to moderate | Tax deductibility depends on use of funds |

| Investment Borrowing | Borrowing to invest without linking to home equity | Higher market fluctuations | Generally deductible, subject to ATO compliance |

Debt recycling is unique because it does not necessarily increase your overall borrowing capacity but changes the type of debt you hold. However, it requires careful structuring with loan splitting, redraw vs offset facilities, and potentially advice from a mortgage broker.

Example Scenario

Consider an Australian couple with a $300,000 home loan. They have stable cash flow and decide to recycle their debt:

| Year | Mortgage Paid Off | Amount Redrawn | Investment Returns | Deductible Debt Proportion |

|---|---|---|---|---|

| 1 | $20,000 | $20,000 | $1,500 | 6.67% |

| 2 | $40,000 | $40,000 | $3,000 | 13.33% |

| 3 | $60,000 | $60,000 | $4,500 | 20% |

Over several years, they steadily replace non-deductible debt with tax-deductible debt. Meanwhile, their investment portfolio generates dividends and potential capital value growth. The couple benefits from tax savings, increased net worth, and a faster mortgage reduction.

Benefits of Debt Recycling

- Tax Deductibility: Converts home loan interest into tax-deductible interest.

- Accelerated Mortgage Repayment: Extra investment income reduces personal debt levels.

- Wealth Creation: Builds an investment portfolio of investment assets such as rental properties, shares, and ETFs.

- Financial Independence: Greater potential for passive income and long-term net worth growth.

- Diversification: Allows Australians to hold a mix of share portfolio, managed funds, and property investments.

Risks and Considerations

- Market Risk: Market downturns or market volatility can cause investment losses.

- Interest Rate Risk: Rising interest rates increase mortgage interest and interest expenses.

- Loan Structure Complexity: Requires careful management of amortising loans, amortisation schedules, and loan splitting.

- Transaction Costs: Brokerage fees and property transaction costs reduce returns.

- Income Stability: Essential for sustaining repayments; consider income protection insurance.

- Tax Compliance: Misuse of redraws or incorrect accounting may breach ATO guidelines.

Who Should Consider Debt Recycling?

Debt recycling may suit Australians who:

- Have significant equity in your home.

- Maintain strong and reliable cash flow.

- Understand borrowing to invest and market fluctuations.

- Have a long-term view and accept capital gains tax on eventual asset sales.

- Want to expand wealth outside super through a trust structure, super investment, or with guidance from an SMSF auditor.

Common Questions and Misconceptions

- Is debt recycling legal and ATO-compliant? Yes, if implemented correctly within Australian Tax Office rules.

- Does it increase the risk of losing my home? Not directly, but poor investment returns could affect overall stability.

- What assets are best? Many choose Australian shares, ETFs, rental properties, or managed funds, often benefiting from franking credits.

- Can I partially recycle my debt? Yes, you can use a split loan for flexible recycling.

- Do I need a professional? Yes. Consider working with a financial advisor, mortgage broker, or firms like Hudson Financial Partners, Dark Horse Financial, or thought leaders like Alex Berlee and Peter Thornhill.

Practical Tips and Best Practices

- Keep clear records of loan splits and offset facilities.

- Use separate accounts for investment debt and home loan debt.

- Regularly review your borrowing capacity, LVR (loan-to-value ratio), and amortisation schedule.

- Protect yourself with income protection insurance.

- Stay engaged with communities like Aussie FIRE via social media for peer insights.

- Factor in additional costs like land tax and property expenses.

Conclusion

Debt recycling can be a powerful strategy for Australian homeowners, combining mortgage recycling, investment growth, and tax savings. However, it carries risks like market fluctuations and requires careful structuring, often with investment advice services. Always seek tailored advice from a qualified financial advisor before making decisions, and consider impacts on concessional contributions or super investment strategies.

Additional Resources

- Australian Tax Office guides on tax deductibility and investment loans.

- ASIC MoneySmart resources on borrowing and investing.

- Financial blogs, books, and insights from the Aussie FIRE movement.

- Trusted advice from firms like Hudson Financial Partners and Dark Horse Financial.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index