In Australia, understanding Fringe Benefits Tax (FBT) is essential for both employers and employees who use company vehicles. As a financial advisor, having a deep grasp of FBT obligations and strategies can help clients reduce unnecessary tax exposure while staying compliant with Australian Taxation Office (ATO) regulations. This Car Fringe Benefits Tax Guide provides a detailed look at how FBT applies to motor vehicles, particularly electric vehicles, plug-in hybrid vehicles, and traditional passenger vehicles.

The Fringe Benefits Tax Assessment Act 1986 governs how employers must pay FBT on certain fringe benefits, including company cars provided for private use. These benefits can significantly impact the taxable value, gross-up rate, and reportable fringe benefits amount on an employee’s income statement. Understanding the implications of Statutory Formula Method, Employee Contribution Method, GST credits, and income tax deductions ensures that clients remain compliant while optimising financial outcomes.

Recent updates from the Australian Government have made FBT more dynamic, especially with the introduction of the electric car FBT exemption, changes to luxury car tax (LCT), and increasing focus on sustainability. This guide will help you navigate complex FBT issues—whether advising on a novated lease, salary packaging arrangements, or managing a fleet of motor vehicles.

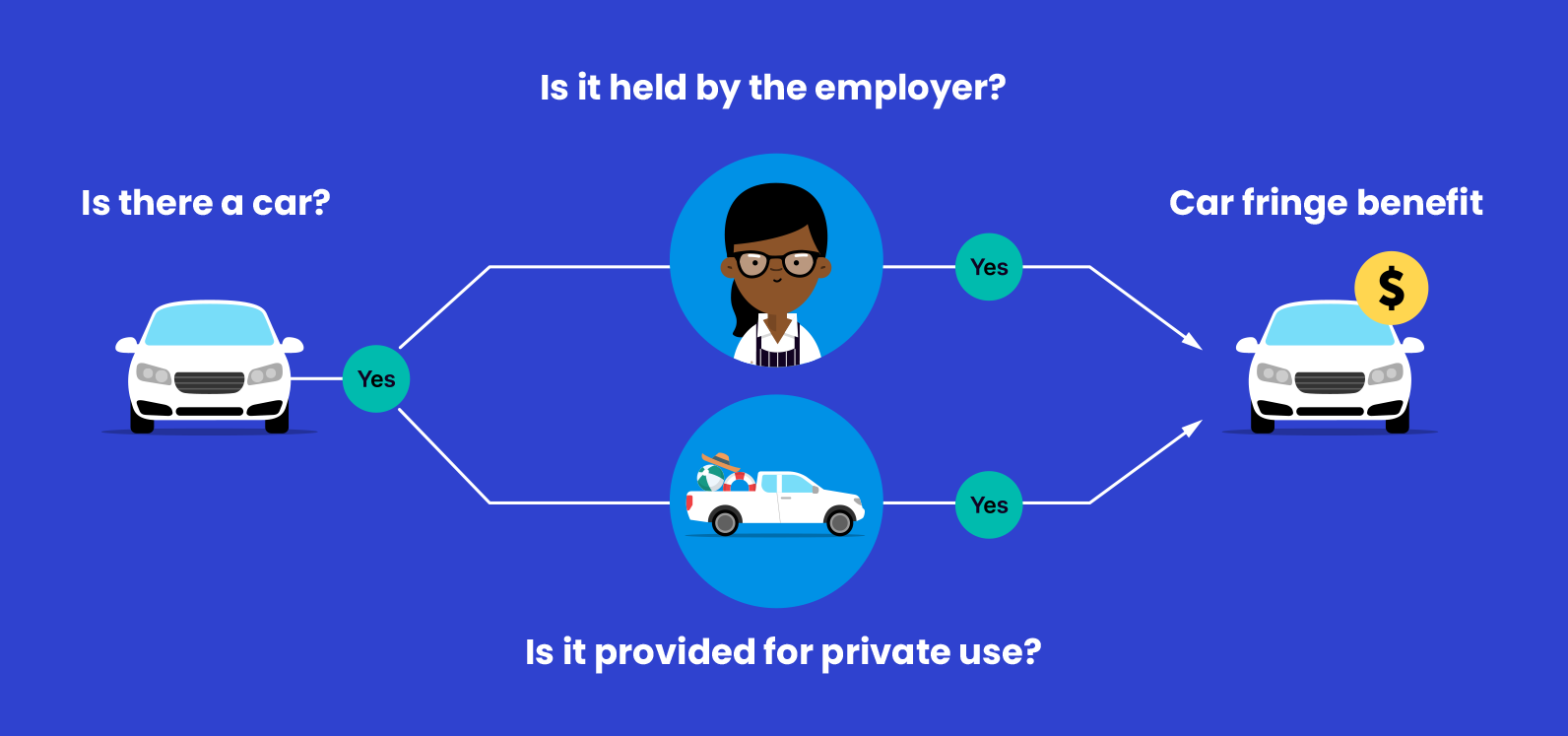

What Constitutes a Car Fringe Benefit?

Definition of a Car

According to the Australian Tax Office, a car includes motor vehicles such as sedans, station wagons, 4-wheel-drive vehicles, and utility trucks designed to carry less than one tonne or fewer than nine passengers. The manufactured design and load carrying capacity determine whether the vehicle qualifies under FBT rules. Some panel vans, emergency service cars, and passenger vehicles may fall within or outside FBT depending on their holding period and private use.

Private Use Examples

A car fringe benefit arises when a vehicle is used for private purposes, including:

- Home garaging: When a company car is kept overnight at the employee’s home, even if unused.

- Driving to and from work: Considered private use under ATO rules.

- Weekend leisure or holiday trips: Personal travel is always taxable under FBT.

Employers must maintain accurate trip data through an electronic logbook or manual records to substantiate business versus private travel. The ATO Practical Compliance Guidelines and Miscellaneous Taxation Ruling MT 2027 outline methods for determining private usage and establishing reasonable odometer readings.

Calculating Fringe Benefits Tax on Cars

There are two main calculation methods under ATO guidance:

1. Statutory Formula Method

The Statutory Formula Method is commonly used for simplicity. The taxable value of the car fringe benefit is determined as 20% (Statutory Rate) of the car’s base value, adjusted for the holding period and routine servicing costs. The base value excludes registration, stamp duty, and insurance.

For example, an employer providing a Tesla Model 3 RWD under a novated lease may calculate the FBT liability using this method. Employers can claim GST credits for eligible expenses and must include the grossed-up value on the employee’s income statement.

2. Operating Cost Method (Employee Contribution Method)

This method allocates costs based on the proportion of private and business use. Employers must maintain a valid logbook for at least 12 continuous weeks in an FBT year, noting trip data, odometer readings, and purpose of each trip.

- Operating costs include fuel, maintenance, insurance, depreciation (using the ATO depreciation rate), lease payments, and interest.

- Employee contributions toward costs reduce the FBT liability and may qualify for income tax deductions.

- The ATO allows manual calculation or the use of digital tools with real-time data.

| Method | Description |

|---|---|

| Statutory Formula | 20% of base value (Statutory Rate) minus employee contributions |

| Operating Cost (Employee Contribution Method) | Actual expenses multiplied by private use percentage |

Exemptions and Reductions

FBT Exemptions

- Electric car FBT exemption: Applies to certain electric vehicles and plug-in hybrid vehicles below the LCT threshold, first held after 1 July 2022.

- Work-related vehicles: Cars used exclusively for business or with restricted private use (like utility trucks or panel vans) may be exempt.

- Not-for-profit employers: Entities such as public benevolent institutions, health promotion charities, and public hospitals can access FBT concessions.

Reductions

- Employee contributions: Employees can contribute to running costs to reduce FBT.

- Accurate logbooks: Maintaining electronic logbooks can reduce the private use percentage, directly lowering the taxable value.

- Fleet discounts: Negotiated leasing company rates and routine servicing can further reduce FBT exposure.

Other Common Fringe Benefits

Beyond cars, employers may offer additional fringe benefits subject to FBT:

- Accommodation allowance and Living away from home allowances

- Entertainment allowance and Entertainment expenses

- Housing benefits and Remote area housing

- Mobile phones and gym membership subsidies

- Discounted loans, superannuation contributions, and employee relocation expenses

- Salary packaged meal entertainment and compassionate travel benefits

Each of these benefits has unique valuation rules under the FBT system, requiring careful management and accurate reporting through Single Touch Payroll.

Step-by-Step Guide to FBT Compliance

- Assess Private Use: Determine whether the car is available for private use based on home garaging and employee access.

- Select Calculation Method: Choose between the Statutory Formula Method and Operating Cost Method.

- Maintain Records: Use electronic logbooks or manual entries to record odometer readings and trip details.

- Calculate Taxable Value: Apply the chosen method, accounting for gross-up rate, GST credits, and employee contributions.

- Lodge Your FBT Return: Submit annual FBT lodgements to the Australian Taxation Office or via the Access Manager portal.

- Review Regularly: Reassess vehicle usage, costs, and any statutory regulations or taxation determinations issued by the Taxation of Fringe Benefits Unit.

FAQs

Q: What is the FBT rate in Australia?

A: The FBT rate is currently 47% on the taxable value of the fringe benefit.

Q: Are electric vehicles exempt from FBT?

A: Yes, certain electric vehicles under the LCT threshold qualify for the electric car FBT exemption if first held after 1 July 2022.

Q: What is considered private use?

A: Any home garaging, commuting, or personal travel constitutes private use, even on weekends or holidays.

Q: What records are needed for the Operating Cost Method?

A: You must maintain a logbook, record odometer readings, note trip data, and substantiate business vs. private travel.

Q: Can FBT be reduced through employee contributions?

A: Yes. Employees can contribute toward vehicle running costs, reducing the FBT liability and possibly claiming an income tax deduction.

Conclusion

For Australians navigating Fringe Benefits Tax, understanding how FBT applies to motor vehicles—particularly under Statutory Formula and Employee Contribution Methods—is crucial. As electric vehicles like the Tesla Model 3 RWD become more popular, the interplay between FBT liability, GST system, and income tax deductions continues to evolve.

Financial advisors play a vital role in helping clients manage company cars, salary sacrificing arrangements, and novated leasing effectively. With careful planning, use of electronic logbooks, and staying current through resources like the Small Business Learning Platform, Tax Academy micro-credential, or LinkedIn profile updates, clients can ensure compliance while maximising benefits.

Whether you’re a business owner, employee, or foreign investor, proactive FBT management ensures you stay compliant with the Australian Taxation Office while optimising financial outcomes across FBT years.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index