A bare trust within the context of a Self-Managed Super Fund (SMSF) is a specialised legal arrangement designed to meet the strict requirements of a limited recourse borrowing arrangement (LRBA). Under this legal structure, the SMSF maintains its position as the beneficial owner of an acquirable asset, such as a commercial property or SMSF investment property, while a custodian trustee (the legal owner) holds the legal title until the loan is fully repaid.

This structure plays a vital role in asset protection, ensuring compliance with superannuation laws and maintaining legal separation between the SMSF and the custodian trustee. For SMSF investors looking to grow their retirement savings through property acquisition, it is an essential setup that protects other SMSF assets from lender claims and prevents a breach of superannuation laws.

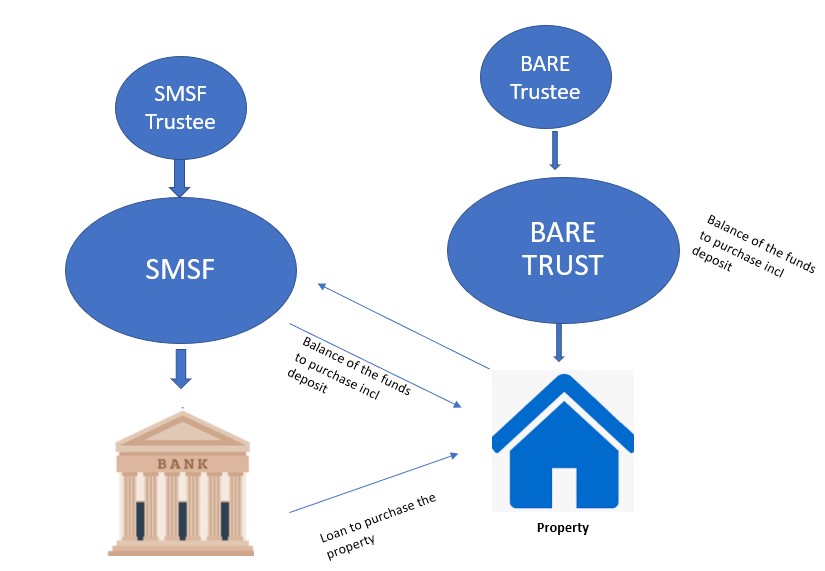

Quick Definitions and Roles

- SMSF: A self-managed super fund where members act as trustees, managing their own retirement savings and making their own investment decisions.

- LRBA (Limited Recourse Borrowing Arrangement): A type of loan where the lender’s claim is restricted to the financed asset, reducing risk to other SMSF assets.

- Bare Trust (Custodian Trust): A type of trust that holds legal ownership of an asset while the SMSF retains beneficial interest.

- Parties Involved:

How a Bare Trust Works in an SMSF LRBA

- Legal Ownership vs Beneficial Ownership: The legal owner (custodian trustee) holds the property title while the SMSF enjoys beneficial ownership, collects rental income, and covers expenses.

- Flow of Funds: All rental income flows directly into the SMSF, which also makes loan repayments.

- Title Transfer: When the loan is repaid, the legal title is transferred to the SMSF trustee without triggering a CGT event.

- Limited Recourse: The arrangement protects other SMSF assets and ensures compliance with super law.

When You Must Use a Bare Trust

- Required for any borrowing arrangement by an SMSF to acquire a single acquirable asset.

- Each purchase requires a separate trust to maintain legal compliance.

- Must be set up before signing a purchase contract to avoid tax consequences and legal issues.

The “Single Acquirable Asset” Rule Explained

- Defined as an identifiable asset, not a bundle of assets.

- Properties with multiple titles may need separate trusts to comply with the house asset rule.

- Examples include strata lots, car parks, and certain fixtures.

What You Can and Cannot Do with Borrowed Funds

- Allowed: Property acquisition, refinancing, paying legal costs, repairs, and maintenance.

- Not Allowed: Improvements that create a new asset.

- Key Rule: Understand the difference between repairs and improvements to avoid SMSF defaults.

Setting Up a Bare Trust: Step-by-Step

- Ensure SMSF deed allows for LRBA and bare trust setup.

- Engage professionals for legal documentation.

- Choose custodian trustee – corporate trustees offer more security.

- Secure finance from SMSF-compliant lenders.

- Execute the bare trust deed before the purchase contract is signed.

- Arrange deposit and property loan approval.

- Complete settlement with property title in custodian trustee’s name.

- Conduct annual mortgage reviews and maintain compliance.

Choosing the Bare Trustee: Individual vs Corporate

- Corporate Trustee: Simplifies trustee setup, title transfers, and ensures continuity.

- Individual Trustee: Higher risk of complications from death, incapacity, or conveyancing.

Compliance, Documentation, and Lender Considerations

- Core Documents: SMSF deed, investment strategy, loan and trust agreements.

- Lender Requirements: Valuation checks, liquidity tests, and asset-based recourse.

- Audit Requirements: Proof of beneficial ownership and proper financial flows.

Tax, Stamp Duty, and Costs

- Income Tax: Rental income and capital gains taxed within the SMSF.

- Stamp Duty: Relief may apply on title transfer.

- Costs: Legal fees, lender fees, and ongoing administration – seek advice from tax professionals.

Practical Examples and Scenarios

- Buying a commercial property via a bare trust.

- Leasing to a related party within legal limits.

- Multi-title property requiring separate entity trusts.

- Renovations using cash instead of borrowed funds.

Common Mistakes and How to Avoid Them

- Setting up the trust after signing the purchase contract.

- Using borrowed funds for non-permitted improvements.

- Incorrect purchaser details on contracts.

- Failing to correctly collateralise properties.

Frequently Asked Questions

- Is a bare trust always needed for an SMSF property purchase?

- Can the SMSF trustee and custodian trustee be the same legal entity?

- Can cash be used for improvements?

- How is legal title transferred back to the SMSF?

- What happens if the property is sold before the loan is repaid?

Governance and Ongoing Management Best Practices

- All transactions must be handled via the SMSF bank account.

- Maintain a compliant investment strategy.

- Work with an SMSF administrator for annual audits and insurance reviews.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalised financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index