Life insurance is a key pillar of financial planning in Australia, providing financial security and peace of mind for individuals, couples, and families. A life insurance policy ensures that your loved ones receive financial support if you pass away or suffer from a terminal illness, serious illness, or Total and Permanent Disability (TPD). Whether you are just starting a family, planning for retirement, or seeking to secure your wealth goals, understanding life insurance policies can help safeguard your future. With the right coverage amount, a life insurer can help cover school fees, funeral costs, mortgage payments, and medical expenses while allowing your family to maintain their lifestyle.

What Is Life Insurance?

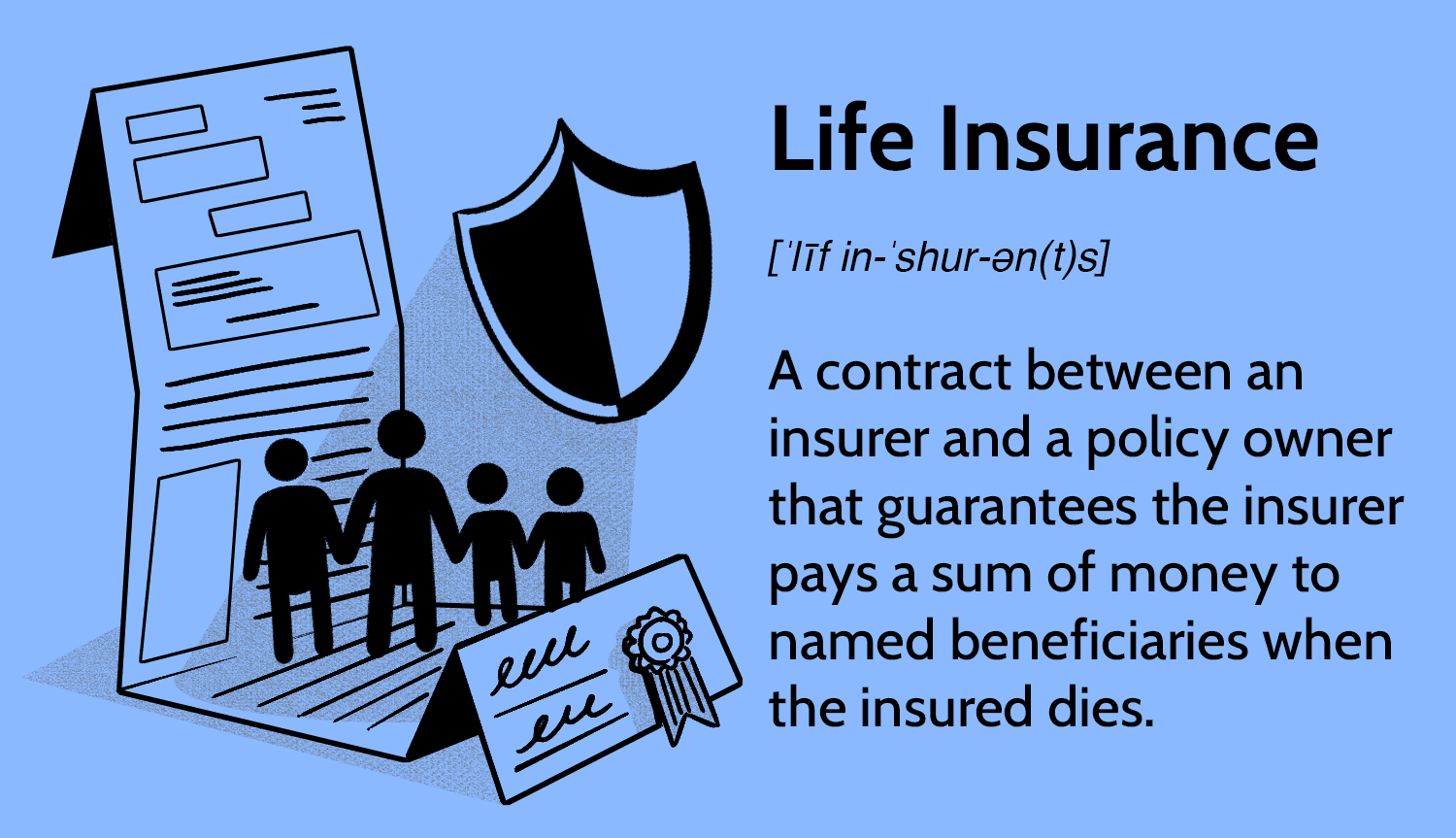

Life insurance is a contract between the policyholder and a life insurer where the insurer agrees to pay a lump-sum payout (the death benefit) to the nominated beneficiaries if the insured person dies, becomes terminally ill, or suffers a serious illness covered by the policy. Some policies also include trauma cover, Critical Illness benefits, or income protection insurance for those unable to work.

Key Components of a Life Insurance Policy

- Policyholder: The person who owns the life policy and manages the Terms and Conditions.

- Premium Payments: The regular insurance cost required to keep the policy active.

- Beneficiary: The individual(s) or estate that receives the benefit amount when a claim process is approved.

- Death Benefit: A lump-sum payout provided when the insured passes away from natural causes or an accident.

- Life Cover Options: May include Total and Permanent Disability Insurance, Trauma Insurance, and Income Protection to provide wider financial support.

In Australia, life insurance policies are often purchased through a superannuation fund, directly from a life insurer, or via a financial planner. Many Australians use a Life Insurance Calculator to estimate the appropriate coverage amount to match their financial debts, savings accounts, and future obligations.

How Does Life Insurance Work?

The claim process and structure of a life insurance policy are straightforward but require careful consideration of your medical history, age bracket, and lifestyle changes. Below is a step-by-step guide:

- Policy Selection: Choose the right type of life insurance—Term Life Insurance, Whole Life Insurance, Universal Life, or Variable Life Insurance—based on your financial planning needs, investment options, and coverage amount. Review the Product Disclosure Statement (PDS), Target Market Determinations (TMD), and Governing Law before purchase.

- Application & Medical Exam: Depending on your medical history, some life insurers may require a medical exam, medical test, or health questionnaire. Your private health fund records may also be requested.

- Premium Payments: Pay regular premiums to maintain the policy. Premiums may vary based on age bracket, health, and insurance cost.

- Claims Process: Upon death or diagnosis of a terminal illness, the beneficiary provides a death certificate and supporting documents to start the claim process. NAB Bereavement Services, for example, can assist families with the paperwork and reimbursement costs.

- Benefit Payout: Once approved, the life insurer provides a lump-sum payout or other benefit amount to cover funeral costs, mortgage payments, school fees, household modifications, or carer support.

Main Types of Life Insurance in Australia

a. Term Life Insurance

Term Life Insurance provides life cover for a set period—10, 20, or 30 years. If the insured dies or is diagnosed as terminally ill within the term, the death benefit is paid to beneficiaries.

- Pros: Affordable premiums, flexible coverage amount, and clear Terms and Conditions.

- Cons: No cash value component; coverage ends when the term expires.

- Best For: Individuals and families seeking financial support for specific timeframes such as mortgage payments, school fees, or major financial debts.

Example: A young couple may use a Life Insurance Calculator to determine a coverage amount that pays off their home loan and provides cash in the bank for their children’s education.

b. Whole Life Insurance (Permanent Life Insurance)

Whole Life Insurance provides lifetime coverage with a cash value component that grows over time. This cash value growth can act like a savings account or investment option.

- Advantages: Guaranteed death benefit, predictable premium payments, and potential cash value growth.

- Drawbacks: Higher insurance cost compared to term life.

- Best For: Long-term wealth goals, estate planning, and financial planning for intergenerational transfers.

c. Universal Life Insurance

Universal life policies combine lifelong coverage with investment options and flexible premium payments.

- Features: Adjustable coverage amount, potential cash value growth linked to market performance, and options for life insurance riders such as recovery insurance or trauma cover.

- Suitability: Australians seeking flexibility and the ability to adjust premiums, cash value growth, and benefit amounts as financial circumstances change.

d. Variable Life Insurance

Variable life policies provide a permanent life insurance structure with investment-linked cash value growth.

- Key Benefit: Policyholders can direct cash value into different investment options for potentially higher returns.

- Risk: Investment performance can impact the cash value component and final death benefit.

Additional Cover Options

- Income Protection Insurance: Provides regular financial support if you cannot work due to illness or injury, with waiting periods applying before benefits begin.

- Trauma Insurance: Pays a lump-sum payout upon diagnosis of a specified serious illness such as cancer, stroke, or heart attack.

- Total and Permanent Disability Insurance (TPD): Provides a benefit amount if you are permanently unable to work due to illness or injury.

- Life Insurance Riders: Optional add-ons to cover lifestyle changes, home modifications, or carer support.

Choosing the Right Life Insurance Policy

When selecting a life policy, Australians should consider factors such as:

- Financial debts, mortgage payments, and funeral costs.

- Current savings accounts, cash in the bank, and superannuation fund balances.

- Age bracket, medical history, and likelihood of lifestyle changes.

- Desired benefit amount and ability to maintain premium payments over time.

Consulting a financial planner can help you navigate Terms and Conditions, Target Market Determinations, and Product Disclosure Statements. A financial planner can also guide you through insurance cost comparisons from providers like MetLife Australia and assist in aligning policies with long-term wealth goals.

Common Myths About Life Insurance

- Myth: “Life insurance is too expensive.”

- Fact: Term Life policies are often more affordable than many Australians expect.

- Myth: “I’m too young for life insurance.”

- Fact: Premium payments are lower when you apply at a younger age bracket.

- Myth: “Single people don’t need life insurance.”

- Fact: Life cover can still pay off financial debts, funeral costs, or provide cash value to your estate.

Frequently Asked Questions (FAQs)

- What is a waiting period?

- The time before certain benefits, such as Income Protection or Critical Illness payouts, become available.

- Do I need a medical exam?

- Some policies require a medical test or health questionnaire, while others offer no-exam options.

- Are life insurance proceeds taxable in Australia?

- Death benefits are generally tax-free, though Governing Law and superannuation fund rules may apply.

- What documents are needed to make a claim?

- Typically a death certificate, medical records, and completed claim forms.

- What is a Product Disclosure Statement (PDS)?

- A document outlining policy Terms and Conditions, insurance cost, and coverage details required by Australian law.

Real-World Applications of Life Insurance

- Family Protection: Covering school fees, mortgage payments, and household modifications for surviving family members.

- Business Planning: Key person insurance ensures business continuity if a partner passes away.

- Estate Planning: Provides financial support for funeral costs, carer support, and cash in the bank for beneficiaries.

- Medical Expenses: Trauma cover can reimburse medical expenses or provide recovery insurance for long-term care needs.

Steps to Purchase Life Insurance in Australia

- Compare Policies: Use a Life Insurance Calculator and Insurance Guide to evaluate insurance cost, coverage amount, and benefit options.

- Read the Fine Print: Carefully review the Product Disclosure Statement, Target Market Determinations, and Privacy Policy.

- Consult a Financial Planner: Seek financial advice to align policies with wealth goals and investment options.

- Complete the Application: Provide medical history, financial information, and identification for underwriting.

- Understand the Claim Process: Familiarise yourself with claim requirements, death certificate procedures, and reimbursement costs.

Glossary of Important Life Insurance Terms

- Cash Value Component: The savings or investment portion of permanent life insurance policies.

- Benefit Amount: The lump-sum payout provided to beneficiaries.

- Governing Law: The legal framework overseeing Australian insurance contracts.

- Product Disclosure Statement (PDS): A document detailing Terms and Conditions of an insurance policy.

- Target Market Determinations (TMD): Defines who the insurance product is suitable for.

Conclusion

Life insurance provides vital financial security and peace of mind for Australians. From Term Life Insurance to Permanent Life Insurance with cash value growth, the right life policy can cover funeral costs, medical expenses, mortgage payments, and more. Whether you are protecting your family, managing financial debts, or planning for long-term wealth goals, consulting a financial planner and reviewing the FSC Website can help you make an informed decision.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index