In Australia’s dynamic financial landscape, there are many investment companies and collective investment schemes available to investors. Navigating this wide range of opportunities can be complex without the guidance of a professional. One vehicle that has become increasingly important in the Australian equity market is the Listed Investment Company (LIC). With their unique structure, professional fund manager oversight, and potential benefits such as franked dividends and franking credits, LICs stand out as a strong option for investors seeking exposure to Australian shares, international equities, and a diversified portfolio. Understanding LICs can help you refine your investment strategies and make more informed decisions along your investment journey.

What Is a Listed Investment Company (LIC)?

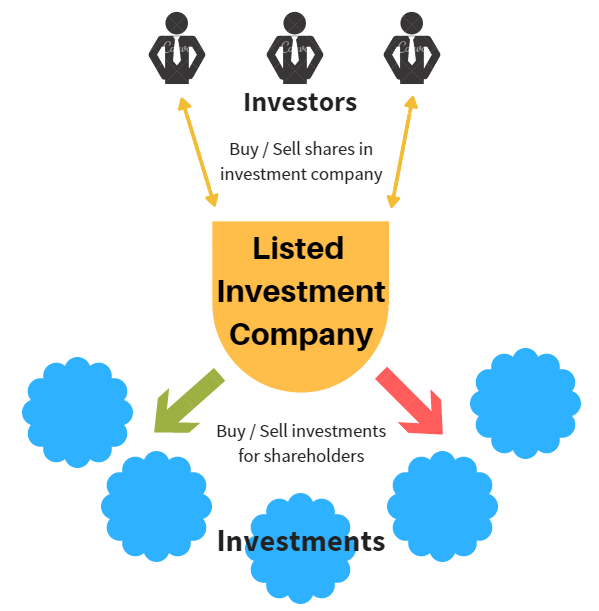

A Listed Investment Company (LIC) is a type of company, structured as a collective investment scheme, that pools money from shareholders to create a diversified portfolio of assets. LICs are traded on the Australian Securities Exchange (ASX), also known as the Australian Stock Exchange, and are subject to regulations under the Corporations Act 2001. They are a form of Listed Investment Vehicle and can be compared with other options such as Managed Funds, Listed Investment Trusts (LITs), and Exchange Traded Funds (ETFs).

Key Features of LICs vs. Other Vehicles

| Feature | LICs | Managed Funds | ETFs / Exchange-Traded Funds | LITs |

|---|---|---|---|---|

| Structure | Company | Trust | Trust | Trust |

| Listing | Yes (on ASX) | No | Yes (on ASX) | Yes (on ASX) |

| Open/Closed-End | Closed-end (fixed capital) | Open-end | Open-end | Closed-end |

| Dividend/Distribution | Dividends, franking credits | Distributions | Distributions | Distributions |

| Management Style | Active approach / Managed | Active approach / Managed | Passive or Active approach | Active approach / Managed |

Unlike open-ended Managed Funds or ETFs, LICs have fixed capital and operate as closed-end vehicles. This structure allows the investment management team to focus on longer term investment strategies, without being forced to buy or sell assets due to inflows or redemptions.

How Do LICs Work?

Step-by-Step Guide

- Capital Raising through an Initial Public Offering (IPO): A LIC is first launched through an IPO, raising capital from investors. At this stage, investors receive shares, and the company becomes listed on the ASX.

- Listing and Share Trading: Once listed, LIC shares can be bought and sold via normal share trading processes, with broking fees applying as they would for other Australian companies.

- Investment Portfolio: The raised capital is invested according to the company’s stated objectives. Portfolios may include Australian shares, international shares, index funds, private equity funds, specialist funds, and even exposure to Indian equities or Chinese property.

- Portfolio Management: The appointed investment manager or fund manager develops an investment approach and executes it using portfolio management and investment risk controls.

- Dividends and Returns: LICs distribute returns to shareholders, often through franked dividends supported by franking levels of the underlying holdings. Investors may also use a dividend reinvestment plan to compound their returns.

The market price of a LIC can differ from its Net Tangible Assets (NTA) or Net Asset Value (NAV), depending on investor sentiment, supply and demand, and the broader investment cycle.

The Closed-End Structure

A key distinction of LICs is their closed-end, fixed capital structure. Unlike open-ended funds, LICs do not issue or redeem shares on demand. Instead, they trade like ordinary Australian companies on the ASX.

Pros and Cons of Closed-End LICs

Pros:

- Stable fixed capital base

- Greater flexibility for long-term investments

- Can pursue actively-selected assets and longer term investment strategies without liquidity pressure

Cons:

- Shares may trade below NTA or NAV

- Lower liquidity compared to open-ended funds

- Market sentiment may influence market cap beyond fundamentals

Income and Growth with LICs

LICs provide investors with two main return streams: dividend income and capital gains. For Australian investors, franked dividends are highly attractive due to their tax efficiency, with franking credits helping to offset personal tax obligations.

Additionally, LICs offer the potential for long term investment performance through capital gains when the share price appreciates. Investors may also benefit from tax incentives such as the CGT Discount when they hold LIC shares as long-term investments.

Advantages of LICs

- Diversified Portfolio: Access to multiple asset classes, from Australian shares to global securities.

- Professional Fund Manager Oversight: Expert investment management teams focused on cost efficiency, management quality, and investment goals.

- Liquidity via ASX: Buy and sell shares easily on the ASX, with transparent verification links and trading records.

- Tax Advantages: Potential benefits from franking credits, capital gains tax concessions, and share buy-back programs.

- Governance: LICs are regulated under the Corporations Act 2001, must hold an Australian Financial Services Licence, and provide Disclosure Documents, Shareholder Agreements, and a registered Australian Company Number.

- Shareholder Engagement: Active dialogue with the investor community and Shareholder Voice forums.

Risks and Considerations

Like all investment vehicles, LICs carry risks:

- Market Risk: Exposure to movements in the S&P/ASX 200 Index, S&P/ASX 200 Accumulation Index, and global markets.

- Premium/Discount Risk: Shares may trade at a discount or premium to NTA or NAV.

- Manager Risk: The quality of the fund manager and investment management team significantly affects returns.

- Fee Structure: Ongoing management fees, management expense ratios (MERs), and performance fees.

- Liquidity Risk: Shares may be harder to trade in thin markets.

Investors should always review Disclosure Documents, check for verification emails when trading online, and align LICs with their fund objectives and investment goals.

LICs vs LITs, ETFs, and Managed Funds

It’s important to compare LICs with other Listed Investment Vehicles:

| Feature | LICs | LITs (Investment Trusts) | ETFs (Exchange-Traded Funds) | Managed Funds |

|---|---|---|---|---|

| Structure | Company | Trust | Trust | Trust |

| Listing | Yes (on ASX) | Yes (on ASX) | Yes (on ASX) | No |

| Capital Base | Fixed capital | Fixed capital | Open-ended | Open-ended |

| Management Style | Active approach | Active approach | Passive or Active approach | Active approach |

| Distribution | Dividends + franking credits | Distributions | Distributions | Distributions |

Each vehicle—LICs, LITs, ETFs, and Managed Funds—serves different roles depending on the investor’s investment approach, risk tolerance, and desire for exposure to certain asset classes.

How to Invest in LICs

Investing in a LIC requires setting up a brokerage account and participating in the Australian equity market.

Step-by-Step Process

- Research: Evaluate performance history, investment strategies, fee structure, and management quality.

- Select a Broker: Choose a broker (online or traditional) to access the ASX. Expect broking fees when trading.

- Place an Order: Buy shares at the prevailing market price or set a limit.

- Monitor Performance: Track against benchmarks like the S&P/ASX 200 and S&P/ASX 200 Accumulation Index.

- Exit the Investment: Sell shares via your broker, considering capital gains tax implications and timing within the investment cycle.

Case Studies: Well-Known LICs in Australia

- Australian Foundation Investment Co. Ltd (AFIC): One of the largest LICs in Australia, with holdings across blue-chip Australian companies such as Commonwealth Bank of Australia and Woolworths Group. AFIC has a reputation for strong governance and long term investment performance.

- Argo Investments Limited: Another major player, focusing on long-term investments in high-quality Australian companies with strong Environmental, Social and Governance (ESG) credentials.

- WAM Capital Ltd: Known for its active approach and focus on high-performing companies.

- BKI Investment Company Ltd: Offers investors exposure to a range of Australian shares with a consistent dividend track record.

- MCP Master Income Trust: A specialist fund structured as a Listed Investment Trust, giving exposure to private credit markets.

- Brickworks Limited: Not an LIC, but often discussed in investor circles due to its cross-holdings and market significance.

FAQs

Q: Why do LICs trade at a discount to NTA?

A: Market sentiment, management reputation, and the broader market analysis can drive share prices below NTA.

Q: Are LICs good for beginners?

A: Yes, LICs can be a great entry point due to their diversified portfolio, but investors should always consider their personal risk tolerance.

Q: How are LIC dividends taxed?

A: Franked dividends provide access to franking credits, reducing double taxation. Reinvesting through a dividend reinvestment plan is also common.

Q: What costs should I expect?

A: Management fees, MERs, and performance fees may apply. Always review Disclosure Documents before investing.

Q: Do LICs support ESG?

A: Many LICs now integrate Environmental, Social and Governance (ESG) factors into their investment strategies.

Conclusion

For Australian investors, Listed Investment Companies represent a compelling option within the universe of Listed Investment Vehicles. They offer a way to build wealth through a diversified portfolio, access professional fund manager expertise, and benefit from franked dividends, capital gains, and long-term investments. Whether investing in established LICs like AFIC, Argo Investments Limited, or BKI Investment Company Ltd, or exploring specialist options like MCP Master Income Trust, it’s essential to align LICs with your investment goals, fund objectives, and broader investment strategies.

As always, remember that all investments carry risk. Investors should assess their tolerance for investment risk, review Disclosure Documents, and seek advice from a licensed financial advisor with an Australian Financial Services Licence before proceeding.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index