Introduction

Debt recycling is an advanced wealth-building strategy that transforms your home loan—a non-deductible debt—into tax-deductible investment debt. This approach is widely used by Australian homeowners, couples, and families seeking to accelerate mortgage repayment, take advantage of tax deductions, and build long-term wealth through income-producing assets. It effectively turns your existing equity in your home into a foundation for borrowing to invest in growth-oriented assets.

When structured properly, a debt recycling strategy can deliver tax benefits, generate passive income, and enhance your financial position without requiring significant additional savings. Using a split loan, offset account, or line of credit home loan, you can gradually convert non-deductible debt (your mortgage) into deductible debt tied to investment assets such as shares, investment properties, or managed funds. Working alongside a qualified financial adviser or mortgage broker ensures your approach remains compliant with ATO rules and maximises tax deductibility under Australian tax law.

What Is Debt Recycling?

In Australian personal finance, debts are generally classified as either deductible or non-deductible. Your home loan—used for your principal residence—is non-deductible debt, as the interest payments do not attract any tax deductions. However, if you borrow funds for income-generating assets such as shares or rental properties, the interest on investment loans becomes tax-deductible.

Debt recycling works by converting your non-deductible home loan into deductible investment debt. You use your home equity to invest in income-producing assets, such as a share portfolio, investment property, or managed funds. The investment income, franking credits, and tax savings generated from these assets can then be used to make extra principal and interest loan repayments, reducing your home loan faster.

By incorporating loan splits, offset facilities, and a redraw facility, you can clearly separate investment debt from personal borrowings. This ensures accurate record keeping, maintains clear tax implications, and prevents loan contamination—a common issue that can compromise interest deduction eligibility.

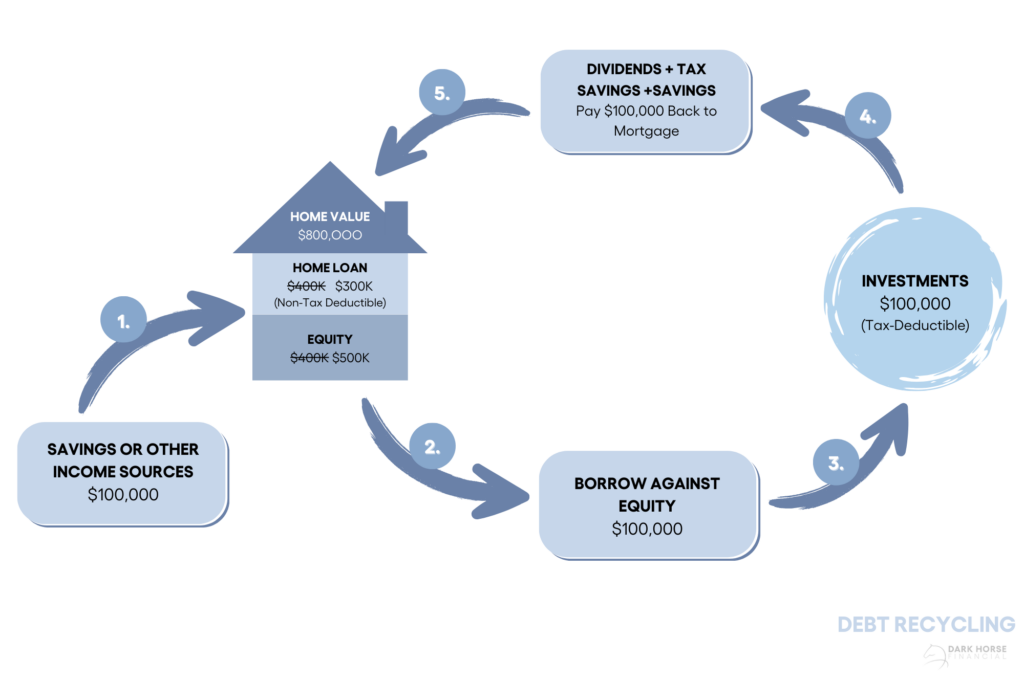

How Debt Recycling Works: Step-by-Step

A. Prerequisites and Who Is It For

A successful debt recycling strategy requires:

- Equity in your home: You must have built-up equity to borrow against.

- Secure income: A reliable income to handle interest payments and market fluctuations.

- Moderate-to-high risk tolerance: Comfort with market volatility, variable rates, and the possibility of short-term losses.

Table: Who Should Consider Debt Recycling

| Profile | Objective | Risk Tolerance |

|---|---|---|

| Young Couples | Wealth creation, long-term investing | Moderate to High |

| Families | Mortgage reduction & financial security | Moderate |

| Share Investors | Maximise tax efficiency | High |

| High Income Earners | Optimise marginal tax rate and wealth building | High |

B. Step-by-Step Process

Step 1: Make Extra Home Loan Repayments

Prioritise reducing your home loan balance through additional principal & interest (P&I) repayments. Use an offset account to minimise mortgage interest and maintain liquidity. Many Australians find using a redraw facility or Line of Credit home loan helps access funds for future investment opportunities without breaking the loan structure.

Step 2: Split Loans or Redraw Equity for Investing

A split loan divides your mortgage into separate portions: one for your home loan (non-deductible) and one for your investment loan (deductible). This setup simplifies record keeping for tax deductibility purposes and helps track your investment performance.

Table: Redraw vs Offset – Key Differences for Debt Recycling

| Feature | Redraw Facility | Offset Account |

|---|---|---|

| Accessibility | Requires lender approval | Immediate access |

| Tax Implications | May mix purposes (risky) | Cleaner for tax reporting |

| Best Use Case | Long-term redraws | Active cash flow management |

Step 3: Borrow to Invest in Income-Producing Assets

Once your equity release is approved, you can use these borrowed funds to purchase income-producing assets. Options include:

- Shares (eligible for franking credits)

- Managed funds or ETFs

- Investment property or rental properties

- Super investment via concessional contributions

The goal is to create investment income streams that can service your interest-only loan or provide tax savings that accelerate home loan repayment.

Step 4: Apply Investment Income and Tax Savings

Redirect all investment income, franking credits, and tax benefits toward repaying your home loan. The more you reduce non-deductible debt, the more capacity you create to borrow again for deductible purposes. This creates a compounding effect that amplifies your wealth creation over time.

Step 5: Repeat the Cycle

As your financial position strengthens, you can continue the debt recycling cycle—repaying, redrawing, and reinvesting—to steadily replace your non-deductible debt with tax-deductible investment debt. This cyclical process supports ongoing wealth building and enhances long-term tax-effective strategy outcomes.

Infographic: Debt Recycling Cycle

[ Make Extra Repayments ] → [ Access Equity ] → [ Invest in Income-Producing Assets ] → [ Use Returns to Pay Down Loan ] → [ Repeat ]Example: Practical Application

Let’s say you have a $600,000 principal-and-interest loan. After several years, you build $200,000 in equity. You decide to draw $50,000 through a loan split to invest in a diversified investment portfolio of Australian shares and managed funds, yielding 7% annually. That $3,500 in investment income, along with tax savings from the deductible interest, goes directly toward paying off your home loan. Over time, this strategy not only accelerates mortgage repayment but also builds a substantial asset base.

Working with a qualified financial advisor or investment advisor (such as GPS Wealth or Hudson Financial Partners) ensures proper structuring, compliance with Part IVA of the tax law, and maximisation of interest deduction potential under Australian Tax Office (ATO) guidelines.

Tax Considerations and ATO Compliance

Under ATO rules, interest on an investment loan is only deductible if the borrowed funds are used for income-producing assets. Accurate record keeping and clear loan segregation are critical to maintaining eligibility for tax deductions. Avoid mixed-purpose borrowing to ensure full tax deductibility of your interest payments.

Key considerations include:

- Capital gains tax (CGT): Applies when you sell investment assets like property or shares.

- Marginal tax rate: Your effective tax savings depend on your tax bracket.

- Medicare levy: Impacts your after-tax returns.

- Super contributions: Additional concessional contributions can complement your debt recycling plan for long-term retirement wealth.

It’s advisable to review your strategy annually with a financial adviser or mortgage broker, ensuring that any interest-only loans, variable rates, or offset facilities remain tax-effective and compliant.

Benefits and Risks

Table: Benefits vs Risks of Debt Recycling

| Benefits | Risks |

|---|---|

| Converts non-deductible debt to tax-deductible debt | Exposure to market volatility |

| Creates passive income streams | Possible negative cash flow during downturns |

| Accelerates mortgage reduction | Requires strict discipline and record keeping |

| Improves tax efficiency | Subject to interest rate and market risk |

| Builds diversified investment portfolio | May not suit those with unstable income |

While the tax benefits and wealth creation potential are compelling, this strategy isn’t suitable for everyone. If your income is unstable or your risk tolerance is low, the strategy could magnify financial pressure during market downturns.

When Is Debt Recycling Not Suitable?

Avoid debt recycling if:

- You have limited home equity or high existing debt.

- Your income is uncertain.

- You cannot tolerate variable rate changes or market risk.

- You lack income protection insurance.

- You expect to sell your property soon.

Also, lumpy assets like property can tie up capital for long periods. Balancing property vs shares is essential for flexibility and liquidity.

Practical Implementation

Successful implementation involves:

- Working with a mortgage broker and financial advisor to design a compliant, tax-effective structure.

- Selecting income-generating assets that align with your risk tolerance and financial goals.

- Using a debt recycling calculator to model cash flow and interest rate changes.

- Monitoring investment performance, interest-only periods, and offset balances regularly.

- Keeping accurate tax records for the Australian Tax Office.

Frequently Asked Questions (FAQ)

- Can I lose money with debt recycling?

Yes. Market fluctuations may reduce the value of your investment portfolio, particularly in volatile markets. - Is debt recycling tax-effective?

When structured correctly, yes—it can maximise tax deductions and interest deduction eligibility. - What happens if interest rates rise?

Your cash flow may tighten. Regularly reviewing with your financial adviser helps manage exposure. - What’s the difference between mortgage recycling and debt recycling?

They are similar. Both involve turning home equity into investment debt for wealth creation. - Are there tax implications if I sell my investments?

Yes. You may incur capital gains tax. Timing and super contributions may reduce your liability. - Can I include super investments?

Yes. Investment outside super and within superConcessional contributions can complement your plan.

Conclusion

Debt recycling can be a highly effective wealth-building strategy for Australians seeking to repay their home loan faster and invest for long-term growth. However, it must be carefully structured to align with your financial position, risk tolerance, and tax implications. With guidance from a qualified financial adviser or investment advice service, you can transform your non-deductible mortgage into a powerful engine for wealth creation and tax efficiency.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.