Introduction

Salary sacrificing is a powerful financial strategy for Australian homeowners that allows you to use pre-tax income to make mortgage repayments, potentially reducing your taxable income and generating significant tax benefits. When structured correctly, salary sacrifice can accelerate the repayment of your home loan while improving your financial position. This guide is specifically for employees, couples, and families in Australia who want to understand how salary packaging and total remuneration packaging can be used to optimise mortgage repayments and tax efficiency.

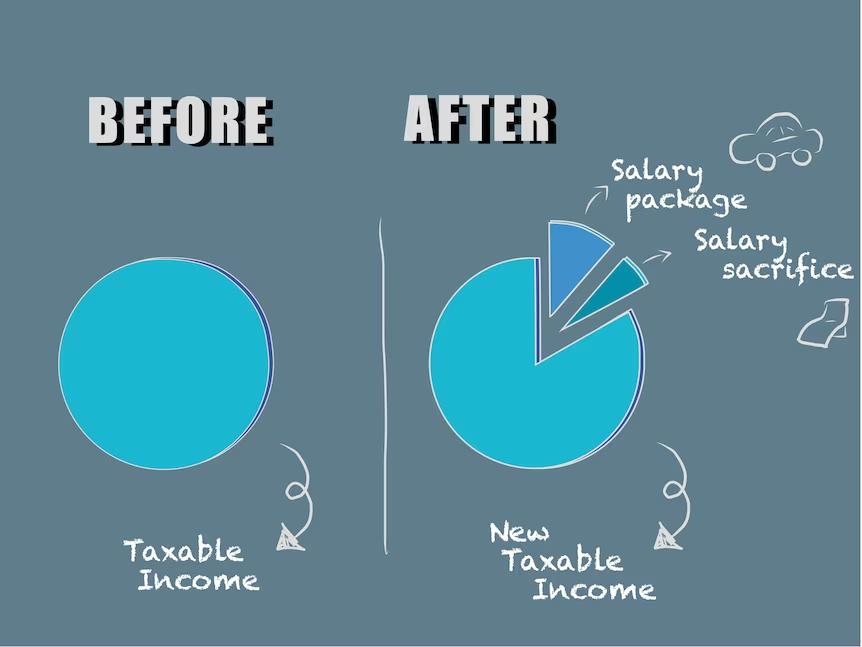

What is Salary Sacrifice?

Salary sacrifice, also referred to as salary packaging or total remuneration packaging, is an arrangement where an employee agrees to forgo part of their pre-tax income in exchange for benefits of similar value. These benefits may include superannuation contributions, motor vehicles, work-related benefits, or, in certain cases, mortgage salary sacrificing for home loan repayments. Employees and employers must formalise a salary sacrifice arrangement to ensure compliance with taxation laws and eligibility requirements.

Not-for-profit organisations, Public Benevolent Institutions, and religious institutions often provide enhanced salary packaging opportunities, including options for mortgage repayments. Public hospitals and public not-for-profit hospitals are typical examples where employees can take advantage of these arrangements.

Can You Salary Sacrifice Your Mortgage?

Eligibility Criteria:

- Employer Types: Generally limited to public sector employees, healthcare workers, charities, not-for-profit organisations, public hospital staff, and public ambulance services.

- Loan Type: Only available for owner-occupied home loans, not investment properties or rent payments.

Important Limitations:

- Payments must go directly to mortgage repayments or a home loan account and cannot be applied to offset accounts.

- Not all employers offer mortgage salary sacrificing, but public hospital employees and FBT-exempt organisations may have more flexible arrangements.

FAQ: Can I salary sacrifice my mortgage with any employer?

No, only specific sectors such as public hospitals, public education institutions, and approved not-for-profit organisations provide this option.

How Does Salary Sacrificing a Mortgage Work?

Step-by-Step Guide:

- Confirm Eligibility: Discuss with your HR department and mortgage broker to verify if your employer allows a mortgage salary sacrifice agreement.

- Set Up Agreement: Draft a formal salary package home loan repayments agreement specifying the pre-tax contributions.

- Direct Payments: Employer makes mortgage payments directly from your pre-tax income, reducing taxable income.

- Top-Up if Necessary: Ensure monthly repayments cover the required home loan amount; top up as needed.

| Action | Who is Responsible | Notes |

|---|---|---|

| Confirm Eligibility | Employee | Check with HR and mortgage broker |

| Set Up Salary Sacrifice Agreement | Employee & Employer | Formalise salary package home loan repayments |

| Employer Makes Payments | Employer | Direct mortgage salary sacrificing payments |

| Top-Up Monthly Repayments | Employee | Ensure full repayment of home loan |

Tax Benefits and Financial Impacts

Using salary sacrificing for mortgage payments reduces taxable income, resulting in potential income tax savings. Pre-tax contributions allow homeowners to pay interest costs faster and reduce the loan term, creating financial flexibility.

Example Calculation:

Salary sacrificing $15,000 per year can reduce taxable income and save thousands in income tax, depending on your income level and applicable rates from the Australian Taxation Office.

Financial Impact:

- Interest Rate Savings: By lowering the principal faster, you reduce interest payments and accrued interest.

- Loan Term Reduction: Accelerated repayments shorten the home loan duration.

- Super Contributions: Adjustments to pre-tax contributions may affect superannuation contributions and employee contributions.

| Income Level | Salary Sacrifice Amount | Income Tax Saved | Interest Costs Saved |

|---|---|---|---|

| $80,000 | $10,000 | ~$3,000 | Varies |

| $120,000 | $15,000 | ~$4,500 | Varies |

Downsides and Considerations

Potential Drawbacks:

- Reduced Gross Salary: May impact super contributions, income protection insurance, and eligibility for future loans.

- Fringe Benefits Tax (FBT): Employers could face FBT obligations, although exemptions exist for public hospital and FBT-exempt organisations.

- Caps on Sacrificing: Employers may impose limits based on FBT caps and Benefit Item Fact Sheets.

Additional Considerations:

- Changes in employment, mortgage broker arrangements, or lenders may affect your mortgage salary sacrifice arrangement.

- The Australian Taxation Office regulates salary sacrifice rules, input tax credits, and taxation of pre-tax contributions.

FAQ: Will salary sacrificing affect future credit applications?

Yes, a reduced gross salary may influence eligibility for other credit products, lines of credit, or loans, as lenders assess your income statement and pre-tax contributions.

Alternatives if Salary Sacrificing a Mortgage Isn’t Available

- Traditional Repayments: Continue normal monthly home loan repayments.

- Superannuation Boost: Salary sacrifice into super contributions, using schemes like the First Home Super Saver Scheme.

- Other Benefits: Consider other salary packaging options, including work-related benefits, car fringe benefit, or education, to maximise tax efficiency.

Real Examples and Case Studies

Case Study 1: Public Hospital Employee

A public hospital worker utilises salary sacrificing to reduce taxable income, maximise pre-tax contributions, and pay off a home loan more quickly.

Scenario 2: Private Sector Employee

Unable to salary sacrifice mortgage repayments, the employee leverages super contributions through the First Home Super Saver Scheme for home ownership savings.

| Scenario | Outcome with Salary Sacrifice | Outcome without Salary Sacrifice |

|---|---|---|

| Public Hospital | Tax benefits, reduced interest costs | Regular tax, standard mortgage repayments |

| Private Sector | Not applicable | Uses superannuation strategies instead |

Frequently Asked Questions (FAQs)

- Can all employees salary sacrifice mortgage repayments?

- No, primarily limited to specific sectors and approved not-for-profit organisations.

- What documentation is required?

- Agreements from employer and mortgage broker.

- Does this impact superannuation contributions?

- Yes, pre-tax contributions may affect super contributions and employee contributions.

- Can I salary sacrifice into an investment property?

- No, only owner-occupied home loans are eligible.

- What happens if I repay my mortgage early?

- The mortgage salary sacrifice agreement may need adjustment or termination.

Final Tips Before You Start

- Verify Eligibility: Check with HR, your mortgage broker, and lender.

- Seek Professional Advice: Consult a financial advisor or an Australian Credit Licence holder for credit assistance.

- Consider Impacts: Ensure salary sacrificing doesn’t negatively affect work-related benefits, car fringe benefits, or essential entitlements.

Resources and References

- Government Websites: Learn about salary sacrificing and tax benefits.

- Not-for-Profit Organisations: Check FBT rules and eligibility.

- Financial Advice Channels: Seek guidance from licensed financial advisers, mortgage brokers, and registered Credit Representatives with a Credit Representative Number.

- Departments and Agencies: Department of Housing and Public Works, Australian Taxation Office.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.