Retirement planning is essential for every Australian—individuals, couples, and families alike. Your super fund plays a major role in your long-term retirement outcomes, and understanding how retail super funds differ from other structures can help you make informed decisions. Superannuation is built on compulsory superannuation guarantee contributions made by employers, combined with voluntary concessional contributions and non-concessional contributions. Whether you’re reviewing your current superannuation fund or considering a change, this guide provides a detailed look at retail superannuation funds and how they fit into Australia’s broader retirement planning landscape.

What Is a Retail Super Fund?

Definition

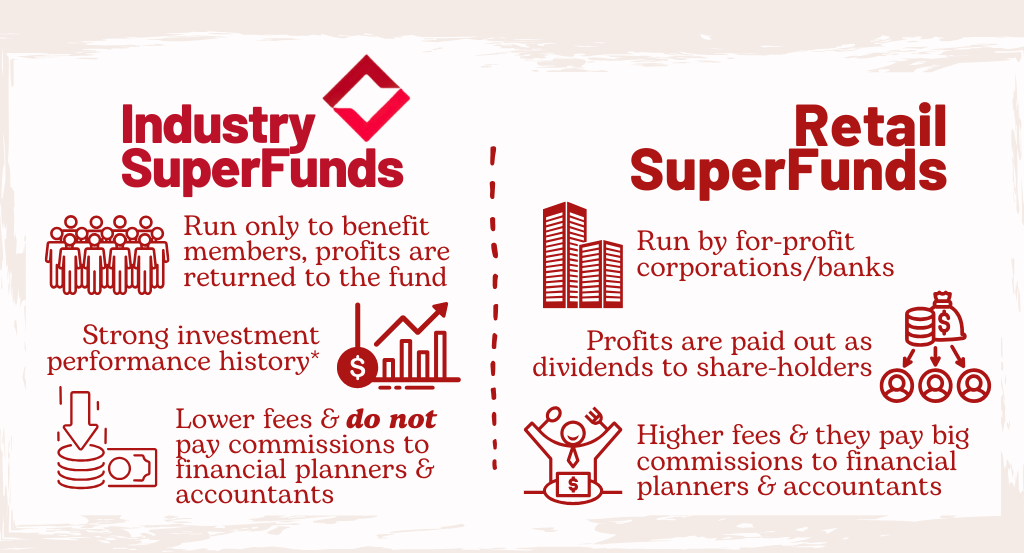

A retail super fund is a type of superannuation fund typically offered by banks, financial institutions, and investment managers. Unlike industry super funds—often linked to trade unions and sector-specific employment—retail super funds are open to anyone.

Who Runs Retail Funds

Retail super funds are operated by financial institutions, investment companies, major banks, and corporate groups. Their fund management strategy generally focuses on delivering competitive investment performance while operating as for-profit organisations.

Profit Motive

Retail superannuation funds operate on a for-profit basis—profits go to shareholders rather than members. This contrasts industry super funds and public sector super funds, which return profits to members.

Comparison Table: Retail vs Industry Super Funds

| Feature | Retail Super Funds | Industry Super Funds |

|---|---|---|

| Management | Financial institutions & investment managers | Not-for-profit organisations linked to unions |

| Profit Destination | Shareholders | Profits to members |

| Membership | Open to all Australians | Often industry-related |

| Fee Structure | Investment fees & administration fees may be higher | Lower average fees |

Key Features of Retail Super Funds

Open Membership

Retail super funds allow any Australian to join—employees, self-employed individuals making self-employed super contributions, expatriates using products like the Australian Expatriate Superannuation Fund, and more.

Investment Options

Retail super funds often provide one of the broadest ranges of investment options, including:

- Australian shares

- International equities

- Balanced Pension and Growth investment strategies

- Private equity

- Evergreen funds

- Sector-specific options

- Conservative, Balanced, Growth, and High Growth choices

- Lifecycle and age-based portfolios

These choices allow members to tailor their investment portfolio in alignment with long-term retirement savings goals.

Fees and Cost Structures

Retail funds typically charge:

- Investment fees

- Administration fees

- Account-keeping fees

- Advice fees (optional)

Some also offer MySuper workplace default funds with simplified structures and competitive pricing.

Insurance Options

Retail super funds commonly include default insurance cover such as life insurance, TPD, and income protection. Member services teams can help tailor this coverage.

How Retail Super Funds Work

Professional Investment Management

Investment decisions are made by qualified investment managers responsible for executing fund management strategies across diversified asset classes.

Asset Allocation

Asset allocation may include:

- Australian shares

- International equities

- Fixed interest

- Property

- Infrastructure

- Private equity

- Defensive assets

Performance Reporting & Transparency

Funds provide:

- Annual statements

- EOFY Investment Updates

- Quarterly performance reports

- Investment news and market summaries

Types and Examples of Retail Super Funds

Major Retail Super Funds

| Fund Name | Notes |

|---|---|

| AMP | Large range of investment options |

| Colonial First State | Long-standing retail provider |

| MLC | Strong corporate super fund presence |

| Mercer | Broad investment menu |

| Vanguard Retail Fund | New entrant offering low-cost indexing options |

Corporate & Public Sector Options

Some employers offer corporate super funds, while government employees may have access to public sector super funds.

Evergreen, Approved Deposit & Eligible Rollover Funds

Retail super funds may utilise structures such as:

- Approved Deposit Funds

- Eligible Rollover Funds

- Evergreen funds (long-term diversified options)

- Retail vs Other Super Fund Structures

Industry Super Funds

Industry superannuation funds—including well-known names like Australian Retirement Trust and Industry SuperFund—operate as not-for-profit funds returning profits to members.

Self-Managed Super Funds (SMSFs)

A Self-Managed Super Fund or Small APRA Fund gives members full control. While offering investment flexibility, they require significant involvement, adherence to Australian Prudential Regulation Authority regulations, and an Australian Financial Services Licence for any advice provided.

Comparison Table

| Feature | Retail Fund | Industry Fund | SMSF |

|---|---|---|---|

| Control | Moderate | Moderate | Full control |

| Fees | Higher, variable | Lower | Variable, dependent on costs |

| Investment Flexibility | High | High | Maximum |

| Management | Professional | Not-for-profit | Member-managed |

Performance and Risk: Key Considerations

Investment Performance

Retail super funds historically lagged behind not-for-profit funds, but competition has improved performance.

Risk Profiles & Investment Strategy

Members should choose an investment strategy aligned with:

- Risk tolerance

- Age & retirement timeline

- Cashflow needs

- Long-term retirement planning

Examples include Balanced Pension options or Investment Growth strategies.

Long-Term Focus

Superannuation is a long-term investment—market fluctuations (e.g., October 07 2025 volatility) should be viewed through a long-term lens.

Fees, Charges & Value for Money

Common Fees

- Investment fees

- Administration fee

- Indirect cost ratios

- Adviser service fees

Economies of Scale

Larger funds often have lower member costs due to scale advantages.

Comparing Fees

Before you change super funds, review:

- Product Disclosure Statements

- Investment menus

- Insurance structures

- Investment fees and administration fees

Choosing a Retail Super Fund: Step-by-Step Guide

What to Look For

- Fee structure

- Member services

- Investment options & strategy

- Insurance benefits

- Risk-adjusted performance

- Whether profits go to members or shareholders

How to Join

- Research: Explore major retail superannuation funds.

- Compare: Use APRA heatmaps and independent comparison tools.

- Apply: Join online using a TFN and ID.

- Consolidate: Roll over other funds, including Eligible Rollover Funds.

Contribution Options

- Superannuation guarantee contributions

- Salary sacrifice concessional contributions

- Personal non-concessional contributions

FAQs

- Are retail super funds safe? Yes—regulated by APRA.

- Can I switch super funds? Yes. Compare investment options and insurance before switching.

- What happens if a fund merges? Your account moves to the successor fund.

- Are contributions tax-deductible? Concessional contributions are.

- Can I start a Transition to Retirement account? Yes, once preservation age is reached.

Pros & Cons of Retail Super Funds

Pros

- Wide range of investment options

- High member services

- Professional investment management

- Strong insurance offerings

Cons

- Higher average fees

- Profits go to shareholders

- Performance varies widely across providers

Conclusion

Retail super funds serve millions of Australians and offer robust investment options, strong member services, and professional management. Whether you’re planning for retirement, considering an account-based pension, or reviewing your investment decisions, understanding how each structure works helps you make better financial choices.

References & Resources

- APRA

- ASIC MoneySmart

- ATO YourSuper Tool

- Major retail fund websites

- Industry Fund Services Ltd publications

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index