In today’s complex Australian financial landscape, understanding a Managed Investment Scheme (MIS) is crucial for individuals, couples, and families seeking diversified investment strategies. Managed investment schemes provide a structure for pooling resources into collective funds managed by professional fund managers, enabling participation in a wide range of underlying assets, including property schemes, Australian equity, fixed interest investments, and Exchange Traded Funds. By exploring the features, benefits, legal framework, and regulatory oversight of MIS in Australia, you can make informed decisions to optimise your Australian financial services investments.

What Is a Managed Investment Scheme?

Legal Definition

Under the Corporations Act 2001 (Cth), a Managed Investment Scheme is defined by several key criteria:

- Investors contribute funds that are pooled for a common investment purpose.

- Investors acquire participation interests in the scheme and rights to benefits from the underlying assets.

- The day-to-day control of the scheme is exercised by a scheme operator or responsible entity, not by individual investors.

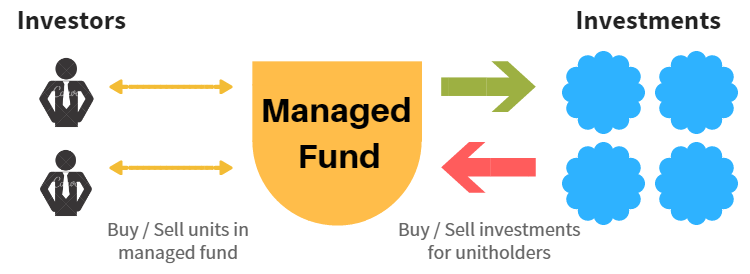

Scheme vs. Company

Unlike Australian companies or traditional corporations on the Australian Securities Exchange (ASX), MIS investors do not have shareholder-style control. Instead, they hold units within a unit trust, managed fund, or limited partnership, as governed by a deed or agreement and subject to the Managed Investments Act.

Common Structures

MIS in Australia may be structured as unit trusts, property trusts, cash management trusts, agricultural schemes, mortgage schemes, or managed investment trusts, often operating under an AFS licence (Australian Financial Services Licence) and compliant with the Corporations Act and regulatory requirements. These schemes may also participate in cross-border initiatives like the Asia Region Funds Passport.

Key Features of Managed Investment Schemes

- Pooled Investments: Combining capital allows access to larger-scale projects, market capitalisation, and international opportunities, enhancing diversification and lowering individual risk.

- Professional Management: A responsible entity or scheme operator with an AFS licence manages investments, using strategies like Algorithmic Management, ESG considerations, and exposure to overseas markets.

- Participation Interests: Investors hold rights to profits and distributions, often detailed in a Product Disclosure Statement (FS88 PDS), including performance fees, Net Asset Value movements, and market price fluctuations.

- Regulatory Oversight: MIS are governed by the Australian Securities and Investments Commission (ASIC) via the ASIC Connect portal, ensuring compliance with section 601EB, the Managed Investments Act, and reporting obligations under Section 68(2).

- Registration Requirements: Schemes exceeding 20 members, or intended for wholesale investors, require registration with ASIC and issuance of an Australian Registered Scheme Number (ARSN).

- Exclusions: Superannuation schemes, life insurance companies, foreign collective investment trusts, and other non-qualifying entities like super funds under the APRA Superannuation Circular or KiwiSaver Act 2006 are not MIS.

Types of Managed Investment Schemes

| Type of MIS | Description |

|---|---|

| Property Trusts | Investment in real estate assets, similar to a Real Estate Investment Trust. |

| Equity Funds | Investment in Australian equity and international stocks. |

| Exchange-Traded Funds (ETFs) | Listed on a stock exchange, tracking indices or sector performance. |

| Agricultural Schemes | Investments in farming, forestry, and ESG-compliant projects. |

| Mortgage Schemes | Investments in mortgage-backed securities or mortgage trusts. |

| Cash Management Trusts | Short-term fixed-interest investments with high liquidity. |

How Managed Investment Schemes Work (Step-by-Step)

- Investor Contributions: Individuals or entities provide capital via Corporate Collective Investment Vehicle structures.

- Pooling of Funds: Contributions are aggregated, creating scale and increasing the Net Asset Value (NAV).

- Professional Management: The responsible entity invests across underlying assets, considering market risk, inflation risk, and performance reports, sometimes using Algorithmic Management techniques.

- Generation of Returns: Investments yield profits, dividends, or income, with potential Tax Implications, including withholding tax for foreign investors.

- Distribution: Returns are distributed based on participation units, in line with the Target Market Determination.

- Investor Exit: Investors may redeem interests subject to scheme-specific liquidity, influenced by liquidity risk and the Insolvency regime.

Legal and Regulatory Framework

- Regulator: Australian Securities and Investments Commission (ASIC) oversees MIS, ensuring compliance via regulatory portal, ASIC Connect, and online services.

- Investor Protection: MIS must separate scheme and operator assets, maintain Certificate of title, land use entitlements, and adhere to disclosure obligations including external administration documents.

- Registration & Reporting: Schemes receive an Australian Registered Scheme Number and must comply with the Asia Region Funds Passport for cross-border operations.

- Tax and Compliance: MIS may flow-through income to Australian residents, subject to reporting to Inland Revenue, SRO Duties Form 58, and compliance under section 275-15.

Benefits and Risks of Managed Investment Schemes

Benefits

- Diversification: Access to multiple underlying assets reduces investment risk.

- Professional Management: Expertise from licensed fund managers, including those overseeing the Global Equity Fund or Sustainable Future Fund, improves Return on Investment (ROI).

- Economies of Scale: Pooled investments reduce transaction costs and improve market positioning.

- Accessibility: Participation in marketplace lending, international ventures, and overseas markets is possible without direct operational involvement.

Risks

- Lack of Control: Investors depend on the scheme operator for daily management.

- Performance Risk: Dependent on market conditions, investment style, and managerial decisions.

- Liquidity Risk: Redemption limitations may apply depending on scheme rules.

- Regulatory Risk: Non-compliance with MIS Review, Managed Investments Act, or regulatory portal directives may impact operations.

Managed Investment Scheme vs Other Investment Structures

| Feature | Managed Investment Scheme | Company Shares | Super Fund | Limited Partnership |

|---|---|---|---|---|

| Control | Managed by responsible entity | Shareholder rights | Trustee control | Limited partner control |

| Structure | Unit trust, property schemes | Company | Trust | Partnership |

| Regulation | ASIC, Corporations Act | ASIC, Corporations Act | APRA, SIS Act | ASIC, Corporations Act |

| Tax Treatment | Flow-through (trusts) | Company tax | Concessional tax | Flow-through (partners) |

| Liquidity | Scheme-specific | Listed/unlisted | Restricted | Scheme-dependent |

Who Should Consider a Managed Investment Scheme?

MIS are suitable for retail and wholesale investors seeking diversification, professional management, and access to sophisticated investment opportunities, including Real Estate Investment Trusts, corporate collective investment vehicles, or agricultural schemes. Considerations include risk tolerance, liquidity needs, and understanding of market price and market risk, particularly for those using super funds or retirement planning frameworks.

Frequently Asked Questions (FAQs)

- What is the difference between a managed investment scheme and a managed fund?

- A managed fund is generally a registered unit trust or managed investment trust, part of the broader managed investment schemes framework.

- Who regulates managed investment schemes in Australia?

- Australian Securities & Investments Commission (ASIC) regulates MIS under the Corporations Act 2001, supported by FS88 PDS, external administration documents, and other disclosure requirements.

- What are the main risks of investing in an MIS?

- Key risks include performance risk, liquidity risk, and reliance on the scheme operator, with compliance requirements detailed in MIS Review and section 601EB.

- How do I verify if a scheme is registered?

- Registration can be confirmed via ASIC Connect using the Australian Registered Scheme Number and reviewing the Product Disclosure Statement.

- Can I withdraw my investment at any time?

- Withdrawal depends on the scheme’s deed or agreement, liquidity, and eligibility criteria for wholesale investors.

Conclusion

Managed Investment Schemes offer professionally managed, diversified investment options across underlying assets, including Australian equity, property schemes, and Exchange Traded Funds. Understanding the legal framework, Corporations Act 2001, regulatory obligations, tax implications, and market risks ensures informed decision-making. Investors should consult a financial advisor, review Product Disclosure Statements, and verify ASIC registration before investing.

Further Resources

- ASIC Managed Investment Scheme Guides

- FS88 PDS Documentation

- ASIC Connect Online Services

- Consult a Licensed Australian Financial Advisor

By understanding the nuances of MIS, investors can confidently navigate the Australian financial services sector, leveraging tools such as Algorithmic Management, Global Equity Funds, and Sustainable Future Funds to optimise returns.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index