A Managed Investment Trust (MIT) is a specialized form of a collective investment vehicle and is considered part of the broader family of unit trusts. They aggregate funds from multiple investors, allowing pooled resources to be professionally managed. The objective is to generate returns through passive income activities such as investments in shares, property, cash management trusts, mortgage trusts, property trusts, share trusts, equity trusts, imputation trusts, balanced trusts, and fixed interest assets.

These vehicles are subject to income tax laws including the Income Tax Assessment Act 1936 and the Income Tax Assessment Act 1997. They provide a framework for trust income, capital gains, and fund payments, while enabling investors to receive income distributions in a tax-effective manner.

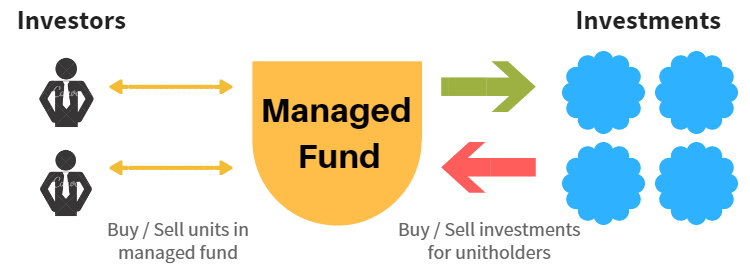

What Is a Managed Investment Trust?

Overview of the Concept

Managed investment trusts are crafted to generate passive income for investors. This can come from dividends on equity investments, rental income from residential real estate, or interest from fixed-income sector securities. MITs differ from other managed funds in that they must meet specific requirements under Division 6, Division 275, and Division 276 of the tax law.

They cannot engage in active trading businesses or large-scale property development. Instead, they concentrate on passive income activities and long-term portfolio management strategies. MITs are commonly used by both local investors and foreign investors, including foreign pension funds seeking exposure to Australian property, equities, and fixed income portfolio strategies.

Comparison Table: MIT vs. Other Common Trusts

| Feature | MIT | Other Trusts / Public Trading Trusts |

|---|---|---|

| Investor pooling | Yes | Varies |

| Passive investments | Required | Not always required |

| Professional management | Yes (Portfolio Manager required) | Sometimes |

| Tax concessions | Yes | Limited/None |

FAQ: Is an MIT the same as a managed fund?

Not exactly. While both involve pooling investor funds, a managed fund is a broader term. An MIT has stricter regulatory requirements, particularly regarding trust income, concessional withholding tax rates, and eligibility under Division 275 and Division 276 of the tax law.

Structure and Mechanisms of MITs

Explanation of Unit Trust Structure

An MIT operates as a unit trust. Investors do not directly own the underlying assets but instead hold units that represent a proportional interest in the trust’s investments. These units entitle holders to trust income and capital gains distributions.

Role of the Responsible Entity/Trustee

The Responsible Entity or trustee must be a licensed professional manager. Their responsibilities include ensuring compliance with income tax laws, corporate governance standards, and fiduciary duties. They also oversee investment processes guided by economic analysis, security evaluation, sector allocation strategy, and fundamental analysis. Many trustees work alongside CFA Charterholders, in-house lawyers, or members of a Board of Advisers to ensure compliance with corporate governance, Practice Compliance & Management, and legal frameworks such as Part IVA, General Anti‑Avoidance Rules, and Safe Harbor provisions.

How MITs Work: Step-by-Step Guide

- Investors contribute funds into the unit trust.

- Fund managers allocate investments across eligible asset classes including investment grade fixed income securities, equities, property trusts, and multi-manager investment trusts.

- Trust generates income passively via dividends, rent, interest, or tax-exempt instruments.

- Income and capital gains are distributed to investors proportionately, with fund payments reported for tax return purposes.

Investment Strategies within MITs

MITs employ both passive and active strategies.

Passive Managed MITs

Passive MITs replicate market indices such as the Bloomberg AGG index or iShares AGG ETF 100%. They might also engage in fixed-income asset allocation strategies, relying on macro environment indicators and economic and capital markets research.

Active Managed MITs

Actively managed MITs rely on research reports, discount cash flow models, investment research, and security evaluation. Managers attempt to outperform benchmarks by leveraging fundamental analysis and economic analysis. Examples include investment providers such as Columbia Threadneedle, BMO GAM, Athena Stock Fund, and CT Global Managed Portfolio Trust.

Income-focused vs. Growth-focused MITs

Some MITs are income-focused, distributing trust income through rent, dividends, or interest, while others are growth-focused, investing in appreciating assets. Hybrid strategies, such as balanced trusts or equity trusts, aim to deliver both.

Table: Strategy Types in MITs

| Type | Asset Focus | Income vs. Growth |

|---|---|---|

| Passive | Index/asset classes | Both |

| Income | Rent, Dividends, Interest | Income |

| Growth | Appreciating assets | Growth |

| Balanced / Multi-manager | Equity + fixed income blend | Both |

Key Benefits of Investing in MITs

- Diversification: Exposure to equities, fixed income, and property investments, reducing risk.

- Professional Management: Access to Portfolio Managers, CFA Charterholders, and professional manager teams.

- Tax Efficiency: MITs provide concessional withholding tax rates for foreign investors and CGT discounts for Australian residents.

- Liquidity: Units in MITs are more easily traded than direct holdings in property or securities.

- ESG Integration: Increasingly, MITs align with ESG (Environment, Social, and Governance) standards.

Taxation of MITs

Overview of Key Tax Rules for MITs

MITs are subject to Division 6 and Division 276. Income is attributed under attribution managed investment trusts (AMITs) and must be reported in tax returns. Compliance with tax measures, foreign resident withholding requirements, and trust loss provisions is essential.

Withholding Tax for Foreign Investors

Foreign investors benefit from concessional withholding tax rates of 10–15%, provided an Effective Exchange of Information (EOI) agreement exists, as outlined by the Australian Taxation Office. Foreign investment from pension funds, ERISA Special Entities, or overseas investment companies often leverages MITs to access Australian assets.

CGT Discount for Australian Residents

Australian residents may receive a CGT discount on capital gains distributed through MITs, making them highly tax-efficient.

Table: Tax Rates and Eligibility for MITs

| Investor Type | Standard Tax Rate | MIT Withholding Tax Rate |

|---|---|---|

| Foreign investor | 30% | 10–15% (with EOI)* |

| Australian resident | CGT discount | N/A |

- (Effective Exchange of Information agreement required)

Qualification Criteria and Compliance

Requirements for a Trust to Qualify as an MIT

- Registered as a managed investment scheme.

- Investments primarily in passive income assets.

- Compliance with non-arm’s length income rules and trust loss provisions.

- Subject to oversight and potential rulings under Notes of Decisions and corporate law precedents like Wilkinson v Springwell Engineering Ltd.

Step-by-Step Checklist: Confirming MIT Status

- Confirm the trust is structured as a unit trust.

- Verify investments are in eligible passive assets (fixed income, equities, property).

- Ensure compliance with Division 275, General Anti‑Avoidance Rules, and Part IVA.

- Seek professional advice from law schools, legal updates, or a Law school resource centre on governance and compliance.

Common Uses of MITs

MITs are widely used to pool investments in residential real estate, affordable housing, equity investments, and fixed-income sector assets. They also form part of global strategies with foreign investment flows and may support pension funds and institutional investors.

MITs are distinct from public trading trusts, money market trusts, and cash management trusts, which may have slightly different compliance frameworks. However, they all serve the purpose of pooling capital for professional management and distribution of trust income.

Risks and Considerations

- Regulatory Changes: MITs must comply with evolving rules, including Division 275 and Practice Compliance & Management standards.

- Tax Risks: Shifts in concessional withholding tax rates, foreign resident withholding, and other tax arrangements can affect distributions.

- Liquidity Risks: Depending on macro environment and market conditions, liquidity in fixed-income asset allocation may tighten.

- Legal Risks: Changing legal interpretations under Scots law, EU Law, or Australian precedents may impact MIT obligations.

FAQs Section

- What is the difference between an MIT and an AMIT?

AMITs (Attribution Managed Investment Trusts) offer greater flexibility in attribution of trust income, allowing more accurate fund payments and adjustments. - Can individuals establish their own MIT?

Technically possible, but compliance with corporate governance, valuation models, and investment process rules often requires institutional expertise. - What assets are eligible for MITs?

Assets such as property trusts, share trusts, equity trusts, fixed income securities, and tax-exempt instruments are eligible, guided by investment research and research reports from sources like Standard & Poor’s. - How are MIT distributions taxed?

Distributions depend on investor type. Foreign investors benefit from concessional withholding tax rates; Australian residents may receive CGT discounts. - What happens if an MIT loses its status?

Loss of MIT qualification can result in higher taxes, stricter oversight, and loss of concessional rates, as seen in prior Notes of Decisions.

Conclusion

MITs provide a structured way to access diversified investments across equities, property, and fixed-income sectors. They offer benefits in diversification, professional management, and tax efficiency while aligning with modern ESG and corporate governance standards. However, compliance with Division 6, Division 275, Division 276, and broader legal requirements is crucial. Always consult financial statements, valuation models, and economic and capital markets research before making decisions.

Before investing, I recommend seeking professional financial advice, supported by legal insights from law schools, practice areas in corporate governance, and financial news sources. Doing so ensures alignment with your unique financial objectives.

Disclaimer: The information provided on this blog is general in nature and does not constitute specific financial advice. It is intended for educational purposes only and should not be relied upon as a substitute for professional financial advice tailored to your individual circumstances. For personalized financial assistance, please contact Brandon Foster via the contact page.

« Back to Glossary Index